SECOND QUARTER 2019

Flexible office arrangements are a growing trend in office markets around the world. Office owners have not historically embraced innovation preferring the stability of the traditional office leasing model over the income generation potential of alternative leasing models.

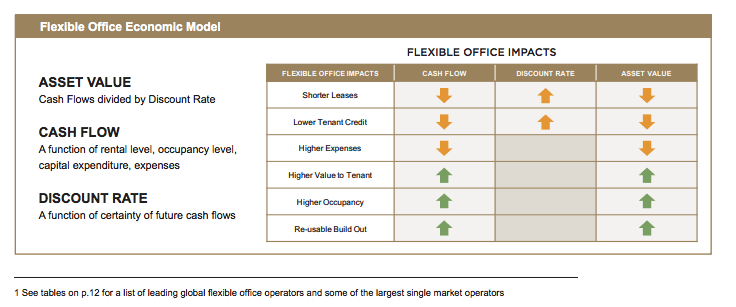

Relatively new entrants to the flexible office market like WeWork, and others, emerged first as tenants of office owners and later as operators and partners with owners. As a group, they are disrupting the status quo of office markets and are becoming intermediaries between building owners and workspace users. Much has already been written about the flexible office movement; but very few of these reports describe the investor’s perspective. That is our focus here. To maintain asset values, owners will need to respond to this new competition for office occupants.

In some cases, owners will need to embrace less certain income streams in the flexible office market for the potential of greater income—either through higher rental rates, risk-sharing leases that optimize net versus gross income, or higher long-term average occupancy rates from positive spillover effects.

In other cases, office owners may avoid the complexities of flexible office tenancy and hold out for lower-risk traditional office leases, even if the net operating income is slightly lower because greater income certainty could do more to drive a higher asset value.

Finding the right balance between stability and income that enhances, rather than diminishes, office asset values should guide how investors react to flexible office trends.

Research & Strategy

Rich Kleinman Managing Director Research and Strategy, Chicago - Americas richard.kleinman@lasalle.com

Zuhaib Butt Associate Strategist, London - Europe zuhaib.butt@lasalle.com

Jacques Gordon Global Strategist, Chicago - Americas jacques.gordon@lasalle.com

Dennis Wong Associate Strategist, Singapore - Asia-Pacific dennis.wong@lasalle.com

Flexible office growth is driven by a growing business need to be nimble, attract talent, and adapt to changing work styles. Businesses are looking for flexible lease terms, space sizes, and space configurations.

However, there are implementation challenges, and the long-term economics of flexible offices are not well-established. The trade-off of cash flow certainty and income levels will drive office market evolution.

We expect additional segmentation of the flexible office market and greater direct owner involvement in the flexible office market. Office owners who ignore the impact of flexible arrangements and their ripple effects on the broader office market are making a mistake.

Similarly, those making long-term commitments without careful evaluation of the economic trade-offs do so at their own peril. Owners should be discerning as to where and when to engage with flexible office tenants, based on the asset and market context, as well as the risk-return strategy.

The length of the holding period and exit strategy should also be a factor when determining the extent of engagement. In this note, we evaluate the flexible office trade-off between income and stability.

We describe the drivers of flexible office growth, segmentations emerging within the flexible office market, the impact it is having on office investment, our expectations for the evolution of office space, and conclude with strategy recommendations for office owners.

A variety of terms are used to describe the provision of office space outside of the historic market norms (which vary around the world). The most commonly used term is “coworking,” but this implies different firms occupying a shared space, and in more and more cases, this is not accurate.

Several brokerage firms have adopted the term “flexible office,” which sometimes applies to how firms use office space within the confines of a traditional lease (e.g., movable furniture or walls).

Taking an owner’s point of view, we focus on how the economic structure and lease terms of work spaces are changing. In this paper, we use both “flexible office” and “coworking” to refer to these changes and sometimes disintermediation in the economic relationship between the building owner and the occupant of the office space.