Various industry commentators are predicting the demise of the traditional bank. The emergence of new competitors and business models is accompanied by sweeping branch closures as digitally savvy customers turn to mobile and online banking.

Banks will continue to be a valuable source of financial services, but institutions will need to choose how to respond to market shifts—whether by leading the future, becoming fast followers, or managing change defensively. Doing nothing is not an option.

Digital-first—often digital-only—startups have joined the market quickly using limited budgets, without the restrictions of existing systems and costs facing traditional banks, to instantly compete against established institutions. Lacking the trust of well-known brands, these startups differentiate themselves with sophisticated, seamless technology that sets a new standard for interactive service. Technology companies have flourished in this space, offering innovative crowdfunding and peer-to- peer financing platforms. These new models raise questions about the fundamental nature of banks and who can provide banking services.

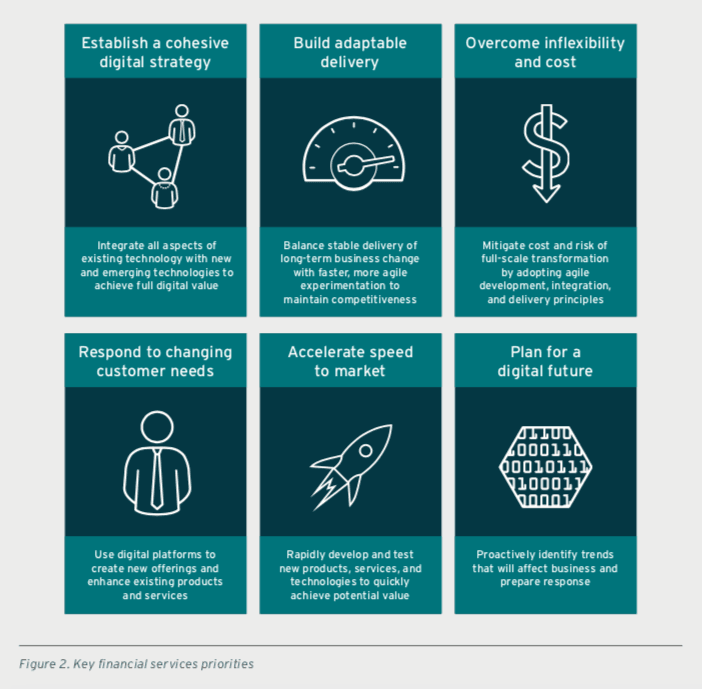

To keep pace with digital-first disruption, banks must apply technology to adopt new delivery channels, simplify spending, managing, and investing money, and introduce products and services that deepen customer relationships. But opportunities are growing faster than IT budgets, and established banks must balance transitioning to fully digital organizations while maintaining business as usual. In addition, new open banking reforms compel banks to restore data ownership to customers and connect existing and emerging IT ecosystems securely.

To rethink operations beyond the branch, banks must prioritize digital engagement for consumers and business customers alike, with a focus on faster, lower-cost payments, seamless integrations, and greater real-time visibility. Achieving these improvements means investing in digital capabilities across front- and back-end systems and expanding analytical capabilities to provide connected insights across customers’ financial journeys. Automated workflows will play a crucial role in transactional efficiency, with business rules providing faster, more accurate retrieval and delivery of data, as well as greater continuity. Building a modern banking platform requires agile integration, an architectural approach based on application programming interfaces (APIs) and effective API management.

Emerging technology providers are both a threat and an opportunity for incumbent insurers. Like fintech companies, insurtech businesses are digitally-native and integrated from the start to provide consumer-centric offerings. These businesses employ personalized, “segment of one” design based on extensive customer insight. They orchestrate services around integrated customer needs, as well as connected object ecosystems with real-time monitoring to reduce risk. From pay-as-you-drive insurance and crowd-sourced insurance pools to on-demand ride- and home-sharing coverage to as-a-service pricing for rarely-used possessions, innovative business models have quickly entered the market.

To support these new models, insurtech pioneers rely on a combination of big data analytics, artificial intelligence (AI), cloud computing, and the Internet of Things (IoT) to gain insight and develop responsive products and services.

Meanwhile, many traditional insurers struggle to deliver the products, services, and experiences customers have come to expect—such as self-service dashboards, faster claims, simpler comparison, and instant enrolment—using outdated systems. Managing a vast amount of content and case processing using niche or non-core applications often results in a partial view of information. This approach does not scale well to handle the influx of data from embedded IoT sensors, drone-generated images, or social media status reports. Patching together systems that were never designed to be integrated leads to duplicated or incomplete data, further stifling innovation.

In this dynamic market, insurers need platforms that connect and extend legacy systems to create a bridge from current, functionally-limited systems to an agile, responsive, and digital future. A technology foundation that can support comprehensive change, complemented by efficient, enterprise- wide approaches, will embed agility into every function.

Capital market firms have traditionally focused on data analytics and high-performance computing (HPC) to reduce transaction times by milliseconds. After transitioning their analytic compute needs, they can now focus on making even faster, smarter trade decisions based on historical and real-time intelligence.

To improve efficiency, revenues, and margins, investment firms need to derive insight from stream- ing data—sourced from a number of external feeds—by rapidly ingesting and indexing data as the transactions are occuring, then visualizing the results.

Data analytics can help investment firms influence how they interact with customers, competitors, regulators, shareholders, and the market as a whole. For example, stock trade information, gathered at various stages of the trading process, can be aggregated for evaluation. Dynamic alerts can notify decision makers when a certain trade crosses a predetermined threshold to begin anomaly identification, a process that will become increasingly proactive with the addition of machine learning capabilities. One of these capabilities, deep learning, can be embedded into streaming trade activity to improve market predictions. In this algorithmic trading approach, systems are built using various methods, including technical analysis, textual analysis, and high-frequency trading.

To reduce the burden of manual compliance, emerging regtech supports compliance with regulatory requirements through monitoring and reporting based on real-time data and analytics. In addition, the growing use of automation is helping asset managers aggressively expand to downmarket customers by sharing insights previously only offered to the most affluent clients. The sector as a whole is shifting from a product-centric view to a client-centric one, with increased investment in customer experiences.

"To improve efficiency, revenues, and margins, investment firms need to derive insight from stream- ing data by rapidly ingesting and indexing data as the transactions are occuring, then visualizing the results."