How can you realize the benefits the energy leaders are seeing? There are four key areas you need to tackle.

The process of reviewing your existing energy use can deliver immediate financial benefits and help you build the case for further investment.

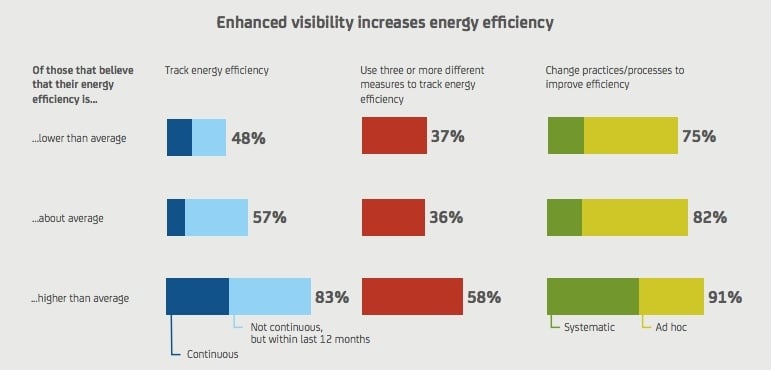

Although the majority of businesses measure and track energy use, there’s significant variation in how well they’re doing this. While many say they measure it, they often haven’t done so within a year or only review it occasionally. Only one quarter of them (24%) say they assess energy use continuously. This means that few organizations have the granular data required to drive operational performance.

While the overwhelming majority of organizations track energy use, not many do it well: many rely on unsophisticated methods and few measure continuously. This gives them little insight into energy efficiency or how it can be improved. Being able to measure energy usage is key to effective management and demonstrating the difference you can make to efficiency over time.

Organizations have a strong impetus for improving their measurement of energy use: those that do are more likely to be energy efficient. Organizations that consider themselves much more efficient than their competitors are much more likely to be continuously measuring their consumption, using multiple methods to do so and are significantly more likely to systematically review and adapt their working practices to improve energy efficiency.

Energy efficient companies continuously track their consumption, use multiple methods to do so, and are systematic in how they implement change.

Greater energy efficiency is strongly linked to having a range of monitoring/tracking tools: the majority (58%) of the most efficient companies use three or more different measures to track energy.

Figure 8: How energy efficient do you believe you are compared to similarly-sized competitors? Is energy efficiency something your organization measures and tracks? How have you measured energy efficiency within your organization? Has your organization ever reviewed or adapted its working practices and processes to improve energy efficiency or costs? [Base: 1,007]

Smart energy solutions, such as wireless sensors and analytics and BMS/building automation systems (BAS), give companies the opportunity to improve energy efficiency. Almost one third of those that have adopted both wireless sensors and BMS/BAS view themselves as much more energy efficient than similarly sized competitors—compared with less than one in ten of those with neither.

Businesses that have adopted smart energy solutions are also more likely to say they are strongly over-performing compared to similarly sized competitors for growth and profitability. Again, the most confident are those that have adopted both wireless sensors and BMS/BAS.

Implementing “a single pane of glass”, which pulls together usage information into one place, can lead to a more integrated approach to energy. Most companies currently lack such insight, with over half (55%) saying they do not have a comprehensive, end-to-end view of their energy efficiency.

Figure 9: To the best of your knowledge, which of the following energy improvements has your organization implemented? How energy efficient do you believe you are compared to similarly-sized competitors? How would you compare your organization’s current performance against similarly-sized competitors for achieving strong financial performance (growth, profitability) [Base: 1,007]

A large cement company, with operations across 50 countries, wanted a solution that would give its plant managers full visibility of how its critical machines were performing. We installed our Panoramic Power wireless sensor technology to measure energy use and pinpoint consumption across different equipment, buildings and plants. This helped the company identify that a conveyor motor was not working correctly, creating a bottleneck. Fixing this delivered a saving of over €200,000 ($233,854) annually at just one location. The data also showed that energy was being consumed unnecessarily across several buildings and plants outside of working hours. Addressing this saved the company some €8,000 ($9,354) a year.

Stories from energy leaders

IoT technologies have transformed how energy use is measured. It’s now practical to measure energy consumption down to the device level, whether that’s a motor in an elevator, a fan in an air-conditioning unit or a freezer in a remote store. Upgrading measurement systems can help you gain real-time insights into energy and operational performance across the whole estate, to understand what is happening at building, floor and device level.

There are many different distributed energy solutions available that you can use to supplement your existing supply. Where are energy leaders investing?

Figure 10: To the best of your knowledge, which of the following energy improvements has your organization implemented? (See page 30 for the solutions included in each category) [Base: 1,633]

Organizations have tended to start their energy journeys by introducing measures that will help them deliver energy efficiency improvements to their buildings, these include HVAC and energy efficient lighting. It’s not surprising that many start here—these are some of the most straightforward solutions, which offer the clearest, and quickest ROI.

Reassuringly, given its importance, two-fifths of organizations say they’ve already adopted wireless sensors and analytics, or BMS/BAS across at least some of their sites. A further fifth, say they’re testing or planning to adopt these solutions.

The business case for thermo-electric generation can be extremely compelling. But unlike something like energy-efficient lighting, it may not be suitable for all companies. Typically, it makes economic sense for businesses with high thermal loads (e.g. hot water, steam, chilled water or hot air) and where electricity costs are high.

Businesses recognize that adopting solutions such as battery storage units and demand response measures can open the door to energy monetization. Nearly all companies surveyed were aware that they could get paid for decreasing demand on the grid at times of peak demand; and the vast majority knew about the incentives to flex their power use based on demand on the grid. Over one third are already selling excess capacity back to the grid, participating in supply-side incentives or demand-side incentives.

Almost one third of businesses have adopted onsite renewables. Clearly adoption of these technologies can be limited by physical considerations — you can’t just stick a wind turbine on your inner city store or add solar panels to your rented branch office. We expect much wider adoption as these technologies and battery storage continue to mature.

While renewables receive the higher profile, more businesses surveyed had adopted integrated heat and power solutions than onsite renewables.

Onsite renewables are an area where collaboration between companies can help. Almost three quarters of businesses believe there are considerable opportunities to share energy infrastructure and generation assets with nearby companies. The most positive about this opportunity are organizations in the US, and companies in the retail and wholesale sectors.

Reed Intermediate School in Newtown, CT, was using 1,958,098 kWh of electricity a year educating hundreds of fifth- and sixth-grade pupils. Although costs are always a factor, the school’s main motivation for going solar was to become more environmentally friendly. Being financed through a Power Purchase Agreement with the Connecticut Green Bank meant the school had no upfront costs, and benefited from immediate savings on electricity. Overall, Reed Intermediate School reduced energy consumption by 39%—and offset CO2 emissions equivalent to 196 tons of waste being recycled each year, instead of sent to landfill.

Many organizations recognize the advantages of energy improvements—but they don’t know where or how to invest. Two thirds of businesses say they don’t know how to make better use of the energy generation assets they already have. Nearly three quarters feel they lack both the commercial and technical expertise needed to realize new opportunities relating to energy. Not many businesses are likely to have the in-house skills to get appropriate aggregation agreements in place, for example.

Taking on new energy solutions can require significant investment. Currently, traditional funding options are most prevalent: two fifths of companies have funded initiatives themselves and one third have used government grants or incentives and bank loans. Other funding methods are starting to be used, such as shared risk models. Payback financing, for example, is a model where investments are funded by a third party typically a supplier— and paid for out of ongoing energy savings or increased revenue, reducing the capex burden on the company.

Leasing and “as a Service” arrangements, while still the exception, are almost twice as likely to be a preferred option among the most advanced companies in our Energy Leadership Model. This supports the belief that funding energy investments through opex will become more prevalent.

For a theme park, based in a rural location, providing power for its waterpark, hotel guests and staff is a sizeable challenge. It recognized that CHP would provide the ideal model for energy and carbon reductions, and cost savings. Under a Power as a Service model, Centrica Business Solutions installed CHP onsite and provides ongoing support. The CHP unit generates energy savings of 12% a year—and as the unit generates power at source, there is very little transmission loss.

Figure 11: In future, which funding methods for energy investments would you prefer to use? [Base: 957, 132]

At the moment, fewer than one in ten companies see “as a Service” as their preferred option for funding the adoption of advanced energy solutions, but that’s likely to grow quickly as businesses become more aware that this option exists. Much of the lack of interest in this type of delivery model can probably be explained by lack of awareness of it even existing. In many fields, from jet engines to computing, the “as a Service” model is now the norm for new equipment.

Cloud computing is a particularly good example of how the “as a Service” model has evolved. While cost reduction remains a driver, in many cases, especially in the enterprise space, companies are turning to third parties for their expertise. We foresee a similar shift in the energy market, with internal energy management teams becoming centers of excellence dedicated to developing strategy, achieving buy-in and optimizing the performance of suppliers.

Energy security and resilience is seen as the biggest business risk, behind only cyber crime. However, attitudes and actions don’t always line up.

Companies are concerned about energy security and resilience. Along with political uncertainty, it’s the most likely to be seen as a substantial business risk after cyber crime. And given the recent focus, and media coverage, of cybersecurity issues, this shows just how real a concern energy resilience is. It ranks above natural disasters and even financial risk.

Businesses are more dependent on energy than ever. And as they depend on power-reliant technology—from the mission-critical hosted applications to electric vehicles—the pressure on supply is likely to increase. Outages could have a significant impact on financial performance and customer loyalty.

71% of organizations agree that the cost of being energy resilient is less than the cost of a power failure.

Many organizations have faced issues relating to energy resilience over the past 12 months. The biggest problem has been interruption to energy supply caused by external factors, such as grid failures due to high demand or extreme weather. Almost one third have also faced problems where internal factors, including equipment failure, have interrupted their supply.

A leading pharmaceutical company’s site in Italy produces a vaccine that must be kept within certain ambient temperatures. If it fails to do this, it must dispose of the vaccine. The company’s task is made harder by the fact that its warehouse is located in an area that suffers from disruption to its energy supplies. Centrica Business Solutions installed a CHP unit which is helping to protect the business by ensuring continuity of supply to the site.

Figure 12: Which of the following do you see as substantial risks to your organization? [Base: 957]

Concerns about energy resilience and the experience of power outages aren’t always driving businesses to rethink their approach to energy. Many organizations aren’t regularly assessing the risks of interruption to their energy supply—only one quarter have done so in the past year.

Real estate companies (24%) are almost twice as likely as those in the travel and tourism industries (13%) to have assessed the risks in the past year.

US-based organizations are the most likely to have assessed the risk of interruptions to supply in the last 12 months: around one third have done so, compared to less than one fifth of British ones. This could be because it’s seen as a bigger threat—almost two fifths of US-based companies said they are significantly concerned about interruption to energy supply due to external factors, compared with one quarter of those in Italy and the UK, for example.

Figure 13: To your knowledge, has your organization ever fully assessed the risk of interruption to its energy supply? [Base: 1,007]

The majority (88%) of companies have an energy resilience plan, but little more than half of them test it regularly and many don’t assess resilience across all locations.

Even when organizations carry out energy resilience assessments, they don’t always do so comprehensively. Assessments at one fifth of companies didn’t cover all locations. And the picture is worse still if we look at organizations without a documented energy resilience plan. In this instance, around three fifths of those companies that have conducted resilience assessments didn’t assess all sites. In contrast, the vast majority of companies with more advanced approaches to energy conduct assessments and do so across all locations.

A leading wine and transportation service provider needed to maintain customers’ inventories in a climate controlled environment, 24/7. It decided to upgrade its portable backup power generator to a permanent installation. The operation was located near sensitive wetlands with noise restrictions, necessitating the use of a high-quality, fully sound-proof enclosure. Due to the urgency of the project, Centrica Business Solutions ensured delivery, setup and full commissioning of the generator within six months.

With greater demands being made on energy, the predictability of supply from central sources is only going to get worse. Many companies are also working with ageing infrastructures that need to be modernized. All of this is making a strong business case for more regular assessments of energy resilience, more rigorous maintenance approaches, back up solutions and reduced reliance on the grid.

The most advanced energy leaders have energy strategies that contribute to achieving their wider business objectives.

Figure 14: Why has your organization chosen to adopt some form of energy strategy? Why do you not have an energy strategy? [Base: 957]

Organizations are adopting energy strategies to provide them with a competitive edge. They’re also being encouraged to do so by the availability of new technologies that have enabled advanced distributed energy solutions. Those that haven’t adopted an energy strategy, typically give “expertise”—such as not knowing how to define an energy strategy or not having the right partners to help— as a reason.

With the exception of the energy intensity of the business and regulation, all these factors are within the control of the business. Interestingly, factors which some companies see as enabling them to develop their energy strategy, some others see as holding them back.

For every business that sees no competitive advantage in adopting an energy strategy, there are almost eight that are investing for that very reason. Similarly, there are 12 times as many businesses that see new technology as an enabler of their energy strategies as those that see it as a barrier.

In 2007, we set ourselves a target to cut global carbon emissions from our property, fleet and travel in half by 2025. By 2015, we’d already cut global property emissions by 44%. In the UK, this involved the introduction of biomass, solar thermal and CHP energy units, as well as the installation of LED lighting at numerous sites. An enhanced BMS allows us to control the energy we consume to increase operational efficiency. In Oxford, UK, we developed a low carbon office capable of obtaining over 30% of its energy from low carbon and renewable technology. In Windsor, UK, we are installing two lithium ion battery units, which will demonstrate how an alternative power source can improve resilience.

In the United States, we have installed energy monitoring sensors across our major offices as well as solar panels on two New Jersey properties, in one case coupled with Battery Storage to optimize and monetize the energy flexibility of that location.

For many organizations today, their energy strategy goes no further than a statement of intent. To accelerate your journey, you need to formalize your plans and show how your energy initiatives will impact the business and how you’ll measure this. Creating a link between your energy plans and your business strategy is an important step towards becoming an energy leader.

Figure 15: How important are the following topics relating to your organization’s use of energy? [Base: 864]. For those areas where there is some detail in your energy strategy at present, are there specific targets, actions or budgets set for these? [Base: 631]

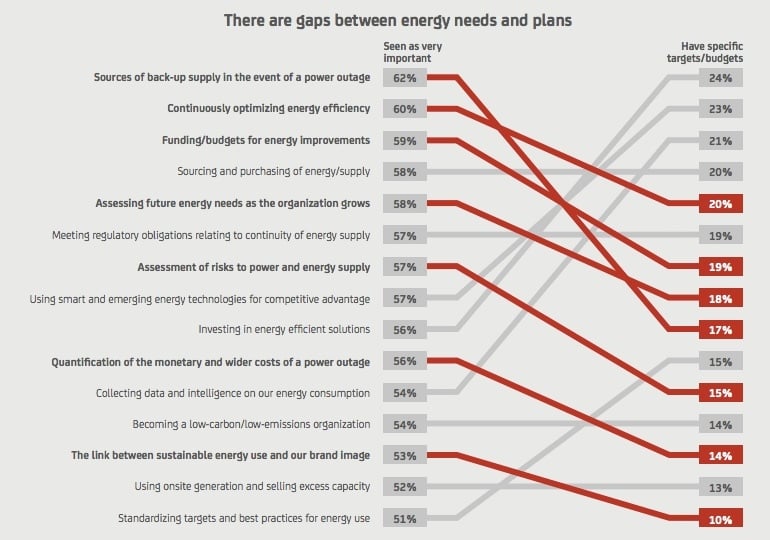

Nearly three quarters of companies say they have an energy strategy. But these are rarely comprehensive or include specific targets, actions or budgets for items they themselves have identified as important to their use of energy. Resilience-related topics, in particular, appear to be under-addressed—possibly as organizations believe these will be the hardest to implement. For example, almost two thirds consider back-up sources in the event of a power outage to be very important but less than one in five have targets, actions or budgets linked to this in their plans.