Index strategies offer a cost-effective, typically diversified way of investing in a collection of securities.

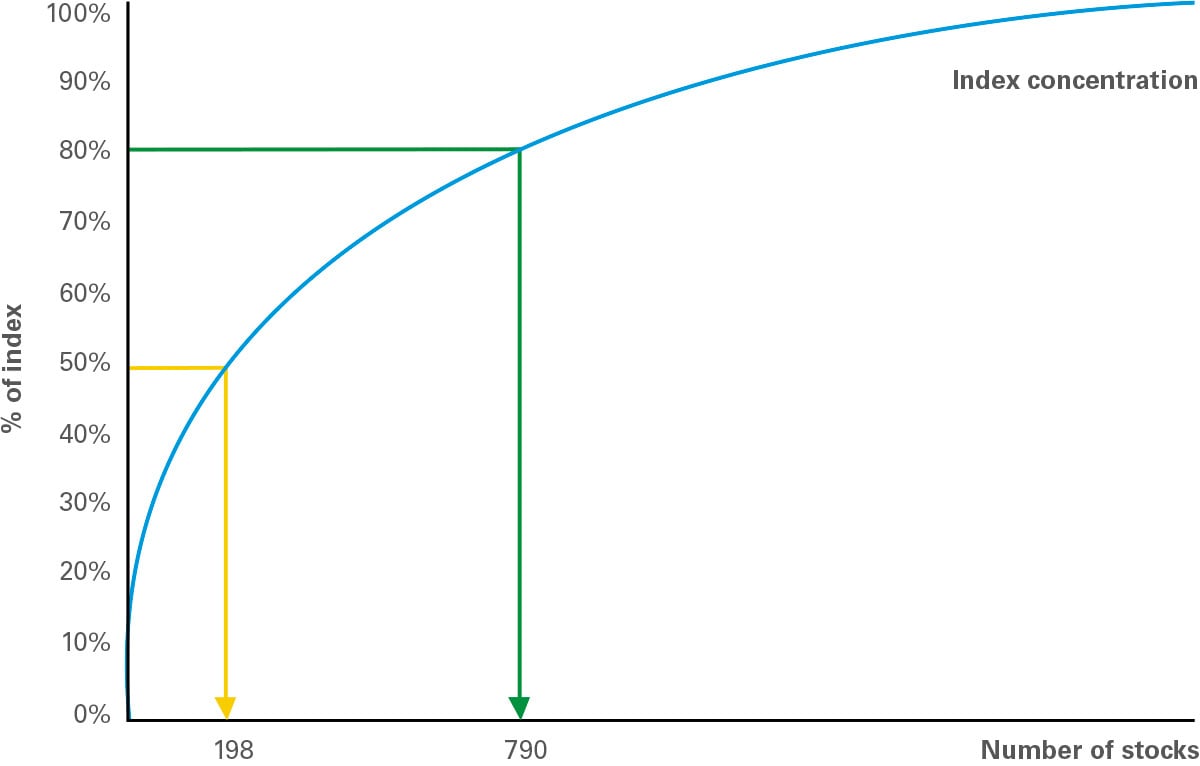

A market cap-weighted index, where each stock in the index is weighted according to its size, means that larger companies carry a proportionally larger weighting than smaller ones, as illustrated opposite. The market cap-weighted portfolio remains a common starting point for long-only investments since it is well-understood and widely quoted.

However, that is not to say that market cap indices are perfect. Market cap indices may be prone to asset price bubbles, biased to past success and risk excessive concentration. As more weight is apportioned to larger, potentially overvalued securities, investors could face significant concentration risk in certain stocks and sectors.

Factor-based indices represent an alternative method of constructing an index. As with any index, factor-based indices use a set of rules to identify a group of securities. However, rather than constructing the index purely based on the basis of company size (as with market cap indices), the rules aim to identify groups of companies with shared characteristics that align with a targeted factor such as low volatility or value.

Source: FTSE, for illustrative purposes.

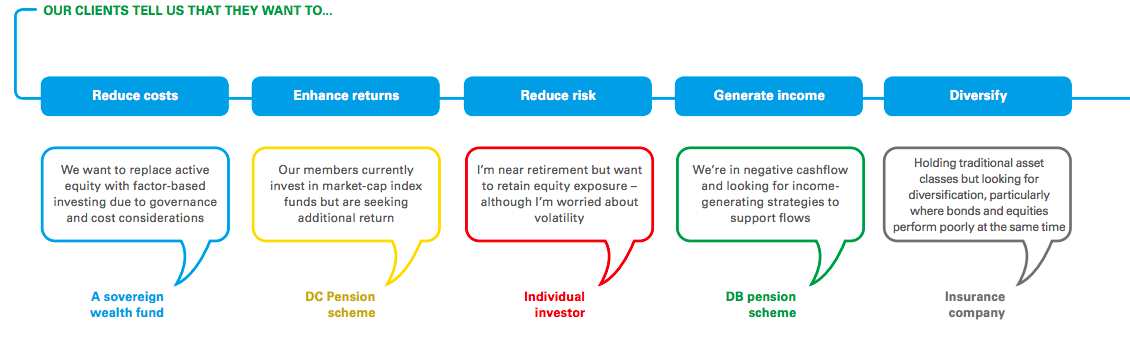

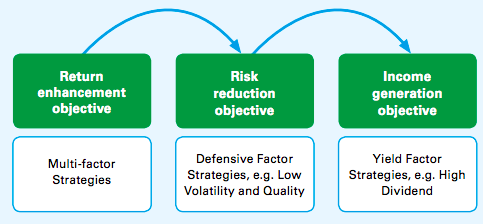

Defined Benefit schemes that are looking for a higher return than market-cap equities, with less downside risk to smooth the deficit reduction journey; wellfunded schemes might consider low volatility strategies while those in cash outflow mode may look at yield factor strategies.

Defined Contribution schemes that are looking for higher return for members during the growth phase, while limiting the risk of poor investment outcomes. The factor exposures could potentially change throughout the lifecycle as shown in the chart below (e.g. pre-retirement where risk reduction is the primary objective and post-retirement when it’s income generation).