Global policy is changing. How will the markets respond?

One of the key themes we identified in the past few quarters was the turning point in monetary policy in developed markets

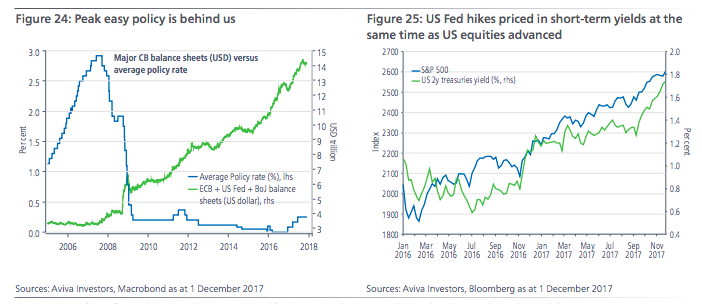

While this was very obvious in the United States as the Federal Reserve started to remove accommodation by hiking rates, it is important to note that peak accommodative policy in Japan and in the Eurozone is probably now behind us. Indeed, within our investment horizon, both the European Central Bank (ECB) and the Bank of Japan (BoJ) are likely to start reducing some of the extraordinary support they have provided, albeit very gradually. And this makes sense – we expect global growth to be in the region of 4 per cent in 2018, causing the global output gap to close more quickly. The pick up in underlying fundamentals has been particularly stark in the Eurozone, but also in Japan. And at the same time, the ECB and the BoJ are still running quantitative easing and negative rates policies. If we are right on our central scenario and inflation rises moderately next year, then markets might have to price in both central banks initiating exit from easy policies. All in all, peak monetary easing is behind us, and this could have significant consequences on financial markets (Figure 24).

Rather than being concerned by the removal of extraordinary monetary policy accommodation, we think it should be welcomed. It is happening because the underlying economic background is strong enough to generate that change in stance. If we look at what is happening in the US for example, Federal Reserve policy is leading to higher yields in short-term government bonds. But this has been accompanied by higher equity prices as underlying earnings growth keeps improving (Figure 25). So the central bank is responding to an improving situation in the real economy. In 2018 we expect to see more movement in this direction.

Markets will be quick to respond once they sniff that change is coming. One example in 2017 was the move higher in the Euro exchange rate, ahead of the ECB announcing reduction in asset purchases. Hence, one of the key objectives for investors next year will be to build scenarios incorporating this turning point in monetary policy and identify underlying investment opportunities.

For much of the past decade, markets frequently moved up or down in response to external factors such as political risk or shifts in monetary policy, a phenomenon that has come to be known as ‘risk-on, risk-off’. Investors moored in safe havens when the macroeconomic environment worsened, then paddled back towards riskier assets when the clouds cleared. But in equity markets at least, this dynamic has begun to change. Since the beginning of 2017, the correlation between stocks within major indices has dramatically broken down. Equity performance is increasingly a reflection of corporate strengths and weaknesses rather than extrinsic circumstances, a development that has big implications for investors.

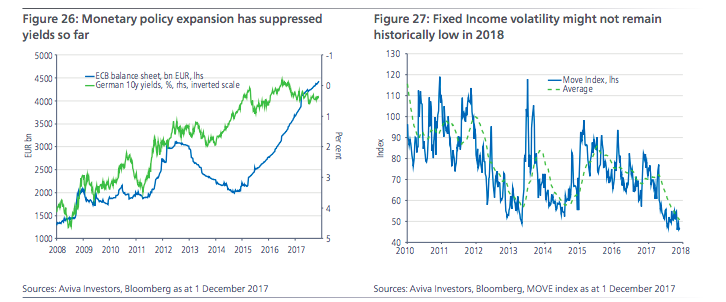

We expect this to remain the case in 2018, and to move beyond equities and into fixed income markets. As we have highlighted in previous editions of the House View, while equity dispersion has risen sharply, fixed income dispersion is still rather low. This divergence is partly a function of the outsized impact of monetary stimulus on credit. By buying bonds and holding interest rates low, central banks spurred a flow of capital into riskier parts of the market, causing spreads to tighten. With the likely turn in monetary policy, this support could start to be removed in the coming year (Figure 26).

In addition to correlation, a key factor next year is likely to be asset market volatility. Across asset classes, volatility has been deeply suppressed this year – we think these historically-low levels of volatility are unlikely to persist, particularly in fixed income. Absent exogenous shocks and within our central scenario, we do not expect the volatility regime to spike higher – but to normalise to the cyclical position of the global economy.

With the beginning of the removal of extraordinary support from central banks, fundamentals are in the driving seat. In some asset classes, like equities or currencies, dispersion can be observed. Earnings growth outlooks and sector allocation matter again for equity allocations, while in the current market environment currencies tend to price early on changes in monetary policy (e.g. Euro response to the ECB) or structural changes (pound sterling and Brexit). Fixed income assets might respond more aggressively to a transition away from being driven by extraordinary monetary policy to being more fundamentally driven. This means that on top of a potentially higher volatility regime, higher dispersion within fixed income should also be expected.

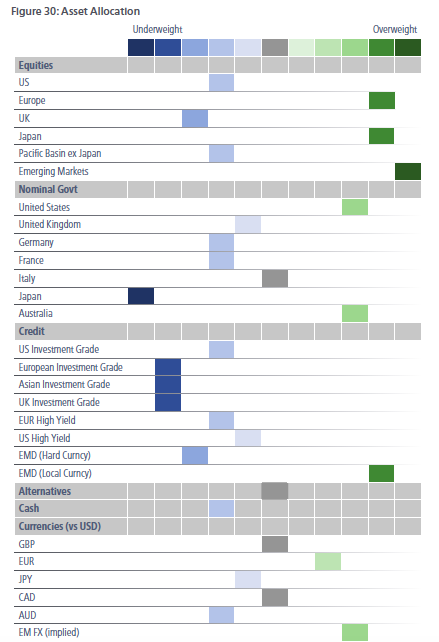

We think next year duration is most at risk. Valuations remain very expensive in markets like Eurozone core fixed income, or Japanese fixed income – or even European corporate credit. While central bank policy has been a key driver for those assets, it is likely to change within our investment horizon. Given our outlook on global growth and on inflation, we think parts of the fixed income asset complex are mispriced when considering underlying fundamentals (Figure 27). In terms of portfolio construction, we continue to run most of our underweights in the fixed income space. The overarching idea underpinning our asset allocation thinking for the year to come is that when investing in a world where fundamentals are strong and peak monetary policy stimulus is behind us, equities should outperform fixed income, and that corporate credit exposure should be an underweight used to protect portfolios. This comes with caveats and specifics within each asset class.

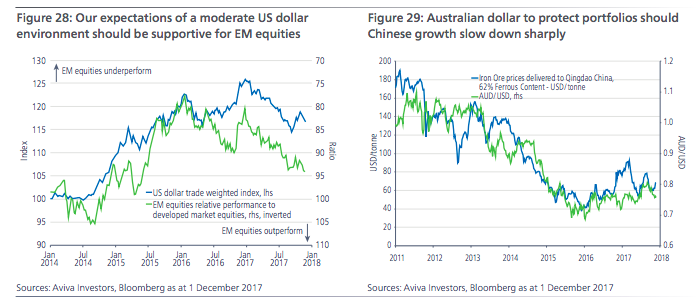

We continue to be overweight equities. Within the equity complex, we prefer emerging market equities (maximum overweight). Fundamentals have been improving in emerging markets as well in terms of economic growth, but also in terms of earnings growth. The outlook from China is probably for slightly lower growth as it seeks to start implementing structural reforms, but this is in the context of a strong global growth backdrop (including in emerging markets), and still attractive relative valuations (Figure 28). We also remain overweight on emerging market local currency debt, as we think higher real yields and positive macroeconomic developments do more than compensate for what we expect to be only a gradual tightening from the US Federal Reserve. We are, however, underweight on hard currency debt as we are concerned by expensive valuations.

We continue to be overweight European equities, which we think are supported by fast improving macro environment in the Eurozone, but also receding political fears. We also increased our exposure to Japanese equities, as corporates are delivering on the earnings front, and the Japanese economy is showing signs of life. Given the starting point of monetary policy in both those geographies, we think gradual steps towards tighter policies should not derail equity markets. In contrast, we remain underweight on US equities, which we find much less attractive from a valuation point of view.

On the other side of the spectrum, we expect some fixed income markets to be under pressure next year. In particular, Eurozone core fixed income is trading on very expensive valuations. With the macro environment remaining strong and the ECB set to remove monetary support (through QE initially), we think the asset offers poor risk-reward.

We are also underweight Japanese government bonds as yields are extremely low, and there is significant downside risk through a potential revision by the Bank of Japan of some of their policies like yield curve control. We also find corporate credit in both Europe and United States to offer little expected return going forward (both are underweights), in absolute terms for Europe and relative to other markets in the equity space for US credit. European Credit in particular is threatened by the end of QE in the Eurozone.

In terms of portfolio construction, we maintain an overweight position on Treasuries at the long end of the curve to protect us should we be wrong in our central scenario. We also have a long position in Australian bonds to balance the risk we take in the emerging market space, as the former should do well in a risk scenario where Chinese growth slows sharply down. (Figure 29).

Sources: Aviva Investors, as at 1 December 2017