Looking ahead at the global markets

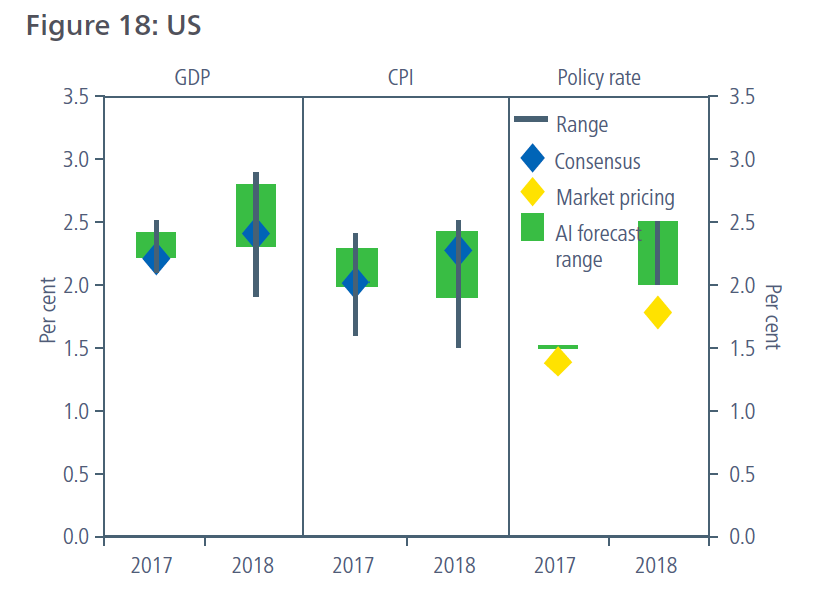

The US economy picked up pace over the course of 2017. Looking ahead, we expect growth to be a little higher next year, with the mix a little more tilted towards investment. The period of softer inflation earlier in 2017 seems to have largely passed. Indeed there appear to be some nascent signs of a further modest pickup in inflation over the coming months. We expect the annual core CPI inflation rate to move back above 2 per cent by mid-2018.

Source: Bloomberg, Aviva Investors, as at 1 December 2017

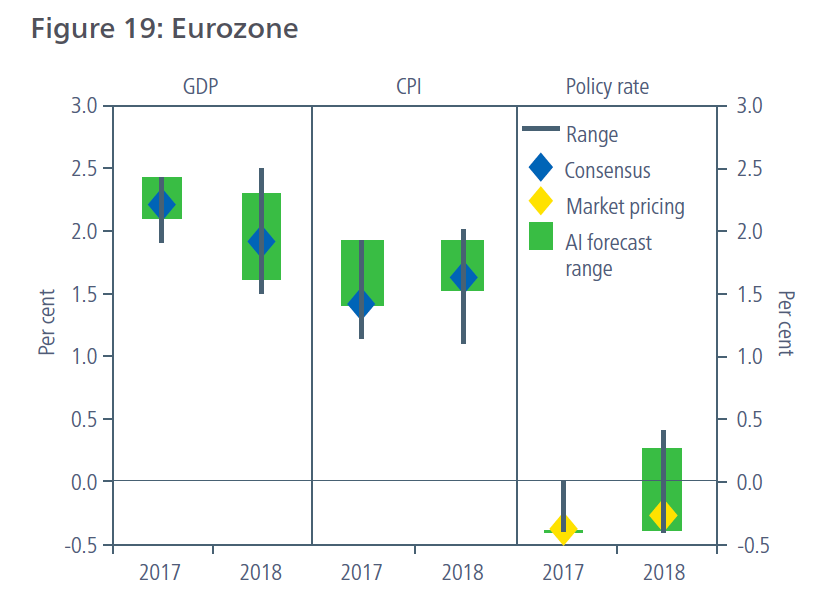

Eurozone business surveys and consumer sentiment readings continue to go from strength to strength, suggesting no imminent moderation in the present boom. Even so, GDP growth should slow a little next year, partly because of the 15 per cent rise in the euro exchange rate in 2017 and partly in anticipation of tighter policy eventually. The kicker from accelerating world trade growth is also likely to fade somewhat. But this is no bad thing – although inflation is subdued for now, the combination of well above-trend growth and super-loose monetary conditions cannot continue indefinitely

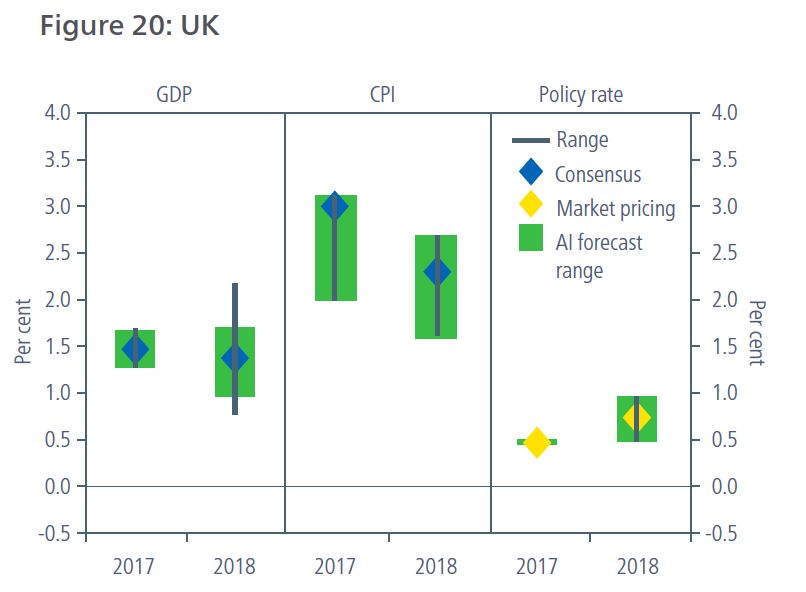

The reassessment of trend growth in the UK from 2 per cent to around 1.5 per cent represents a massive change to the UK's supply-side potential. After 10 years, GDP will now be almost 6 per cent lower than it would otherwise have been: effectively Britain would rather have “lost” three years of growth. Over the shorter term, current growth is sluggish, but at least positive. Some sentiment indicators – both business and households – are fragile and local downside risks are overshadowing the positives from the global upswing. It is not all Brexit-related, but that shadow looms large.

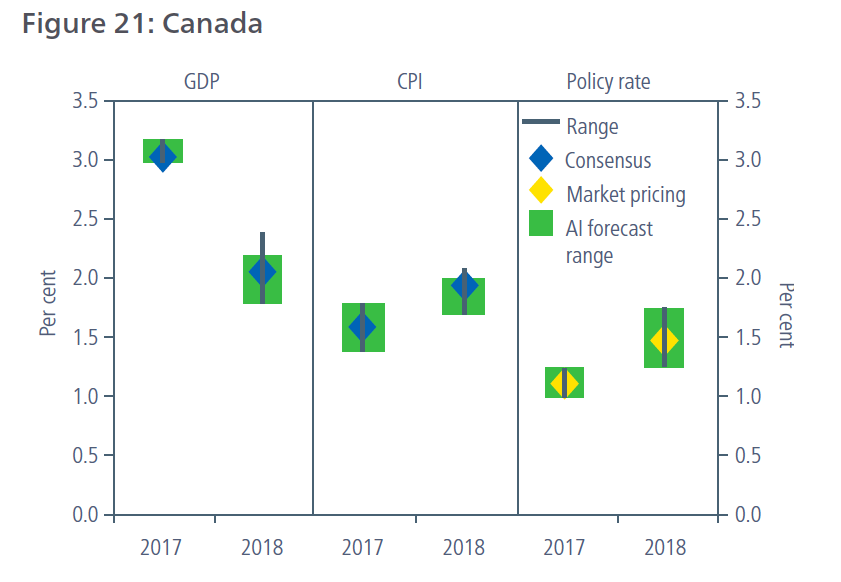

Growth surprised to the upside in 2017, leading the Bank of Canada (BoC) to hike rates twice to 1 per cent. Looking forward to 2018 the rate of growth is expected to moderate to around 2 per cent from 3 per cent. Despite strong growth, inflation has remained below the target and although expected to pick up in 2018, the impact of rate hikes in 2017 and the appreciation of the Canadian dollar will be headwinds to a significant acceleration. The BoC is therefore expected to move more cautiously from here and in particular will be watching wage growth and household debt.

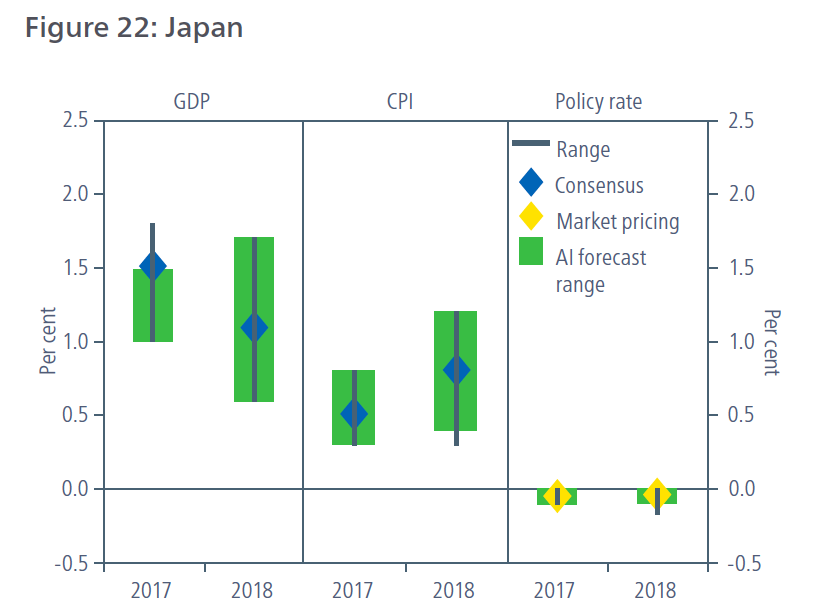

Amid a strong global growth backdrop, the Japanese economy remains in a good place. While Q3 GDP data showed moderation from Q2, survey data (Tankan indicators, PMIs) continues to suggest brisk expansion heading into 2018. While growth is expected to moderate slightly, reflecting the moderation in key trading partners such as China and the Eurozone, it is still likely to remain robust. Core inflation remains very weak for now, but is likely to pick up modestly as the effects of above-trend expansion and labour-market tightness begin to show themselves gradually.

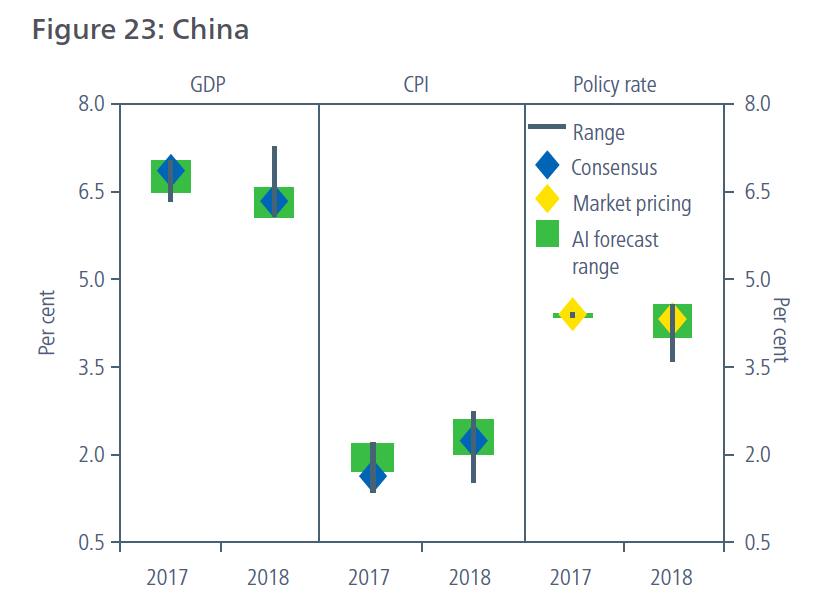

After a year that has seen Chinese growth defy predictions of a slowdown repeatedly, some signs of moderation are emerging as housing market activity continues to cool. But the impact on the wider cycle is likely to be much less pronounced than during 2015-16 as inventories are much lower than in the past. At the same time, wider activity indicators remain robust and survey indicators such as PMIs suggest that the expansion is likely to continue at a modestly slower pace next year. The policy environment is likely to remain broadly supportive as targeted easing mitigates the impact of the ongoing regulatory deleveraging.