Six key points that may be a risk.

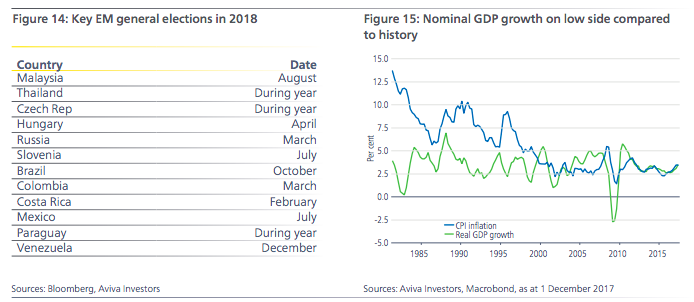

But increased nationalism (“America First”) could easily resurface, especially if Trump doesn’t get his own way on domestic policy. Moreover, the issue is still relevant in many other countries too. It is bubbling beneath the surface across swathes of Europe (AfD representation in fractured German parliament, Brexit aggravations, Italian elections), while the next year or so also sees a number of key elections within important emerging markets (Figure 14). Although it has also quietened down a little, recent episodes between the US and North Korea (and China to a lesser extent) highlight the scope for sudden eruption of conflicts and anxieties in this area.

Although there have been some gyrations in headline inflation rates since the crisis, on average it has remained low and below target in most geographies even while the recovery has continued over much of the last seven or eight years. The combination of a relatively sluggish expansion with continued low inflation has led some to conclude that this is now the normal state of affairs. Secular stagnation is one

variant of this school of thought; supply-side weakness, including very low productivity growth, is another. The impact of technology on the capacity of companies to push through price increases is a third. The recent combination of growth and inflation has been low, but not exceptionally so (Figure 15). A low inflation, low growth environment that persists could permanently change the old policy rulebooks.

As in many other countries the trend GDP growth rate in China is slowing. But China’s size and importance mean that both its growth rate and how the trend slowdown is managed will be watched very closely by financial markets and will have global ramifications. China is attempting to transition to a more open, service based economy. But the combination of the inexperience of its policy-makers, their determination to micro-manage every detail of the economy and society, their ambitious long-term aspirations and the strange demographics as a result of the one child policy means that the scope for upsets and mistakes is significant. There have already been previous episodes of China growth worries that have impacted global markets. A future slowdown could be either a result of transition shocks or could be brought about by policy mistakes. Either way, it would be foolish to ignore the risk of more shocks in the future.

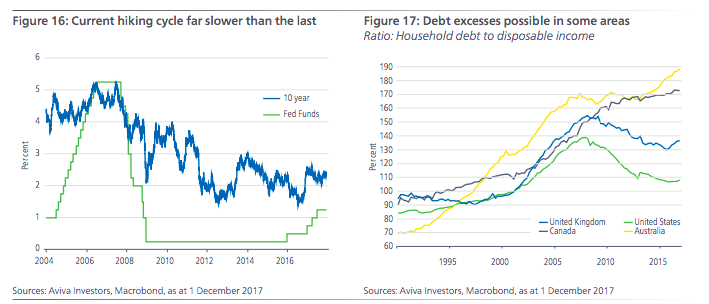

Financial markets continue to believe that the Fed will deliver nothing like its stated intention of seven 25 basis point hikes between now and the end of 2019. They also seem relaxed about the ECB’s glacial journey towards the policy exit and the BoJ’s almost permanent state of assistance provision. The Bank of England has raised rates once, but has hinted heavily that just two more 25 basis point hikes over the next three years is all that should be expected. Against this backdrop, the scope for upside surprises seems an obvious risk to consider. Many have argued that the Fed’s last hiking cycle in 2004/6 (Figure 16) was “too slow” and contributed to many of the problems that came after. The current cycle is less than half that pace. It would not take much for markets to start to worry about upside inflation potential and the need for more active hiking from central banks. This would also threaten the low-volatility regime that has prevailed in recent years.

There is a widespread consensus now that, after a long period in the doldrums, the world has entered a period when policy interest rates will generally be rising. As monetary authorities have gone to great lengths to point out, rate hikes are likely to be “gradual and limited”, especially compared to history. While that is some comfort, we should not be surprised that the exceptionally long phase of ultra-low interest rates has encouraged a wide range of borrowers to take on higher debts. As we shift slowly to a regime of higher interest rates, it is almost inevitable as interest rates now rise, even if the process is very slow, that some of those borrowers will be hurt by the financial burden of higher debt-servicing costs. De-leveraging among households, for example, has been different around the world (Figure 17).

A year ago there were major worries about the possible direction of European politics. The prospect of major gains and increased representation for far-right parties dominated the political outlook for 2017. In the event, such worries proved largely unfounded and political unity (with a centrist flavour) has increased across the Eurozone, helped in part by a “common adversary” in the Brexit negotiations. Even the inconclusive German election result looks likely to result in another coalition with Merkel as leader once more, which should help the revitalised Franco-German alliance to work closely together on the next steps for the Euro project. Combined with the markedly better macroeconomic outlook, this set of conditions should enable important progress to be made on the aspiration of closer integration. Bold words are useful here, but they need now to be followed up with actions and these have been slow in coming. Nevertheless, the fact that the focus of this risk case is on the clear scope for upside surprises in Europe is good news in itself.