Bringing together senior investment professionals from across all markets and geographies.

The Aviva Investors House View Forum brings together senior investment profess-ionals from across all markets and geographies on a quarterly basis to discuss the key themes that we think will drive financial markets over the next two or three years

In so doing, we aim to identify the key themes, how we would expect them to play out in our central scenario, and the balance of risks. We believe that this provides a valuable framework for investment decisions over that horizon.

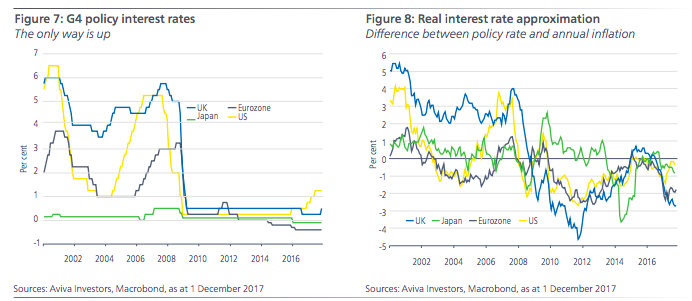

After almost a decade of extraordinary policy stimulus from global central banks, the sands are now shifting. We would contend that the extended period of exceptionally low – or even negative – interest rates (Figure 7), alongside the wide range of “unconventional” monetary initiatives, was essential to help prevent the financial crisis tipping the world economy into a reoccurrence of the Great Depression of the 1930s. Looking ahead to 2018 and beyond, monetary policy drivers for financial markets are set to be very different as the long return journey to more “normal” policy settings is undertaken. The return of trend GDP growth or better and the retreat of deflation fears mean higher interest rates are warranted or will be over the next few years. Post crisis, macroeconomic health was restored initially in the US, so it is no surprise that the Fed has been the first to tighten policy. It remains on a clearly signalled path towards higher interest rates, with one more expected this month and three more in 2018. But the progression will be slow – “limited and gradual” in Central Banker language. Moreover, other central banks are withdrawing their easing stance very cautiously and while we expect others to join the Fed in tightening on a two to three-year view, moves will be measured and very slow by historical standards. We do not expect a pronounced tightening of financial conditions over the next year or so and real interest rates are expected to remain low compared with history (Figure 8). All moves are contingent on a continuation of recent macro trends: ongoing robust GDP growth and a steady and sustained return of inflation to target.

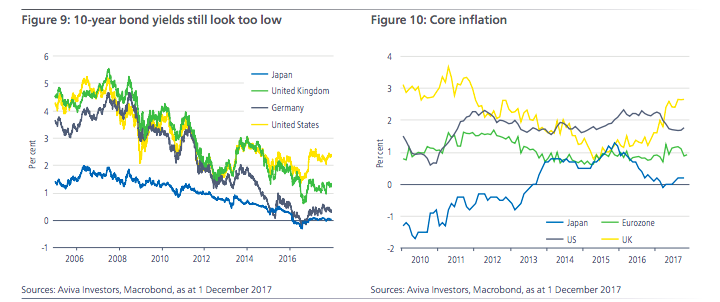

Part of the transmission mechanism for Quantitative Easing (QE) policies to the real economy was the boost they provided to financial asset prices. There are worries in some quarters that the withdrawal of asset purchase programmes around the world (actual or planned) will remove a vital support for risk assets. This is unduly pessimistic in our view – the Fed stopped buying assets three years ago and markets have not collapsed. Looking forward, the ECB is tapering its own purchases in 2018 and the BoJ may also buy at a reduced pace. Although asset prices have benefitted from these programmes, markets are ultimately underpinned by fundamental drivers. These are already reasserting their influence and this can be expected to continue in 2018 and beyond as policy stimulus is withdrawn. Looked at in this light, the much-improved economic outlook and related earnings increases have supported equity markets in 2017 and should do so again, with some qualifications, next year. Sovereign bond yields, on the other hand, may have more of this transition (from policy support drivers to fundamentals) to make over the next few years, especially if we are right about the upbeat growth and inflation outlook (Figure 9). It is also plausible that there could be greater dispersion across fixed income markets as fundamentals reassert themselves, reflecting differing prospects, policy settings and economic conditions.

Fears of secular deflation in the developed world were prevalent during and after the financial crisis, but are now largely absent. However, CPI inflation rates remain generally below Central Bank targets (typically 2 per cent) (Figure 10). This latter feature has persuaded some commentators to argue that inflation will stay permanently too low and that policy, therefore, can remain loose indefinitely. Yet given the imbalance between supply and demand that opened up during the crisis, an extended period of low inflationary pressure was entirely understandable. But the long global expansion since 2009 means that the process of eliminating spare capacity is complete in some countries such as the US and getting much nearer in others, such as the Eurozone. Hence, inflation is expected to move higher on a sustained basis. The evolution for inflation rates in 2017 was not totally convincing in directional terms, with both Europe and the US seeing some modest downside surprises. However, at least some of that was likely to be transitory. Wage inflation has also been subdued, with the G4 average pace still more than a full percentage point lower than the pre-crisis mean (Figure 11).

One of the key themes that we believe will emerge in 2018 and 2019 is a clearer upward trajectory in inflation back to (or even slightly above) those 2 per cent target rates. If that is right, then expectations of sustained positive inflation will become more entrenched and the prevailing environment will distance itself even further from the dangerous deflation frontier and move more compellingly into low, positive inflation territory. Such a development would be an important element in the reappearance of more normal macro-economic conditions.

After the growth scares of 2015, China has enjoyed two years of comparative calm, with GDP goals being achieved or even marginally exceeded (Figure 12). Perhaps more importantly, official growth targets appear to have been subtly downgraded in terms of Government priorities compared to earlier periods. Arguably, being a hostage to fortune where GDP objectives are concerned has been more of a hindrance to Chinese policy as well as to its transition and economic development ambitions. Hence although there are still growth targets implicit in China’s longer term aspirations, they are less front and centre than in the past. (Of course if there were a major downside shock, the Chinese authorities would almost certainly respond aggressively.) This greater flexibility of approach has allowed – and should continue to allow – China to pursue its reform agenda with greater alacrity and on a more systematic basis. Whether explicit or not, China will be aiming for somewhere between 6 per cent and 6.5 per cent growth in 2018. This was also the message that emerged clearly from the 19th Party Congress in October. As well as consolidating his power-base (which should provide greater stability), President Xi modified the economic policy focus in the years ahead, away from the emphasis on growth and towards supply-side reforms (including stateowned-enterprises), deleveraging and the longer-term transformation of China. While some elements of these initiatives will take years to implement and bear fruit, others will have an impact from now on and will help define key parts of the overall global macroeconomic backdrop in 2018 and 2019.

The “One Belt One Road” set of initiatives in particular may well become increasingly important on the world stage. Although what China says and what it does can be very different things, it is an irony not lost on several commentators that China now sounds more amenable to free trade and open markets than Trump’s America.

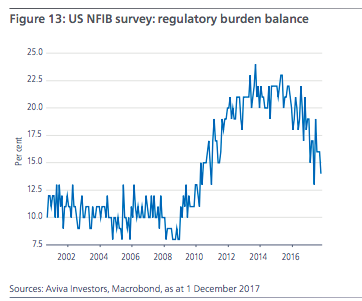

After the inevitable raft of greater financial regulation in the wake of the Global Financial Crisis (GFC), the pace of introduction of additional measures has, just as inevitably, waned somewhat in recent years. This does not mean that we are about to experience a far looser regulatory environment in the near future, but rather that we have probably passed the peak in terms of additional initiatives being announced. Indeed, with the ostensibly market-friendly Mr Trump in the White House, there is even the possibility of a worthwhile reduction in the regulatory burden in some areas (Figure 13). It may take some time, and it has to be said that gauging US policy initiatives on the basis of Trump’s twitter outbursts has not been the most reliable guide to subsequent events. But even a moderate bias towards an easier regulation tilt and less stringent rules would represent an important change to the operating environment for financial (and other) companies. In Europe there has arguably been a greater acceptance of tighter regulation and less momentum behind any moves towards a lighter regulatory touch. But it is also generally accepted that a properly functioning banking system is vital. And in this context it is widely recognised that credit needs to be made available to reputable entities that wish to borrow if the Eurozone recovery is to continue. The latest indications are that credit conditions have eased considerably since the sovereign debt crisis and that lending has picked up. Although it is unlikely to be characterised as looser regulation, the European authorities will wish to ensure that credit continues to flow, without significant hindrance, to where it is needed. When there were more worries about the fundamental health of large parts of the European banking system, this was less of a priority – at such times solvency was more important than liquidity.