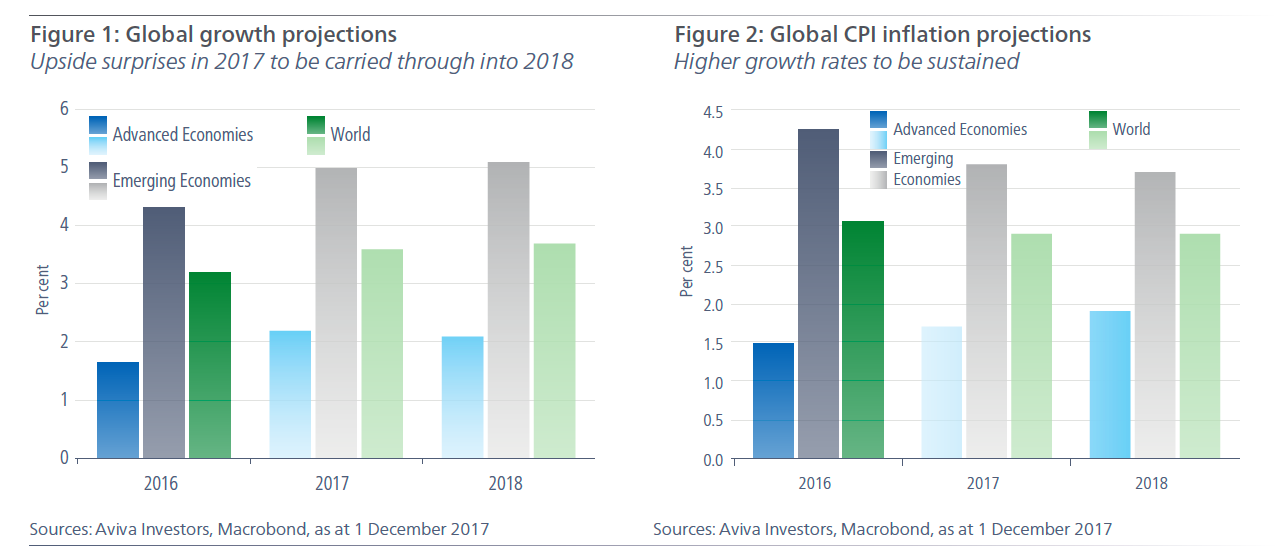

Global growth expected to improve further in 2018

That should see global growth approach 4 per cent, the strongest since 2011 and consistent with a continued reduction in global slack, increased inflationary pressures and a geographical broadening in the removal of extremely accommodative monetary policy. As 2017 draws to a close, it is likely that global growth will finish the year well ahead of where consensus expectations were twelve months ago. That largely reflects much better growth than anticipated in the Eurozone, but also better outturns in Japan and China. It is also in spite of the US failing to deliver on President Trump’s much-vaunted tax reform plans until the end of 2017. It would also be the first time since 2010 that global growth has surprised on the upside, with many forecasters, such as the IMF, raising their projections for 2018 (Figure 1). We have also raised our expectations for 2018, reflecting positive global consumer and business sentiment, limited private sector balance sheet risks and still easy financial conditions. We think the main upside risk is likely to come from the US (on greater-than-expected fiscal stimulus), and the main downside risk likely from a more rapid slowing in Chinese growth.

We expect global consumer price inflation will be little changed in 2018 compared to 2017, with a modest rise in advanced economies offset by a similarly modest decline in emerging market economies (Figure 2). The rise in advanced economy inflation reflects a similar increase of around ¼ per cent across the major economies over the course of next year, with the United Kingdom the only exception. Those increases reflect the lagged effect of the reduction, and in some cases, elimination of spare capacity, that has seen wage growth rise steadily. A further steady rise is expected in 2018, with that imparting further modest upward pressure on inflation. In some economies, such as the US, the impetus for a somewhat larger increase in inflation may come from the potential non-linear effects of an extremely tight labour market. But structural headwinds make it unlikely for inflation to spike higher. Our growth and inflation outlook is consistent with a gradual removal of policy accommodation, with the Federal Reserve leading the way with further rate hikes, but with other central banks likely to move towards tighter, rather than looser policy. In the Eurozone we expect asset purchases to end in September and in Japan we see the potential for the Bank of Japan (BoJ) reviewing its policy of yield curve control (YCC) if core inflation rises above 1 per cent. The outlook for the Bank of England is highly dependent on developments in the Brexit negotiations next year, which have the potential to move policy in either direction. Elsewhere, there is potential for rate rises in Canada, Australia, New Zealand, Sweden and Norway in 2018.

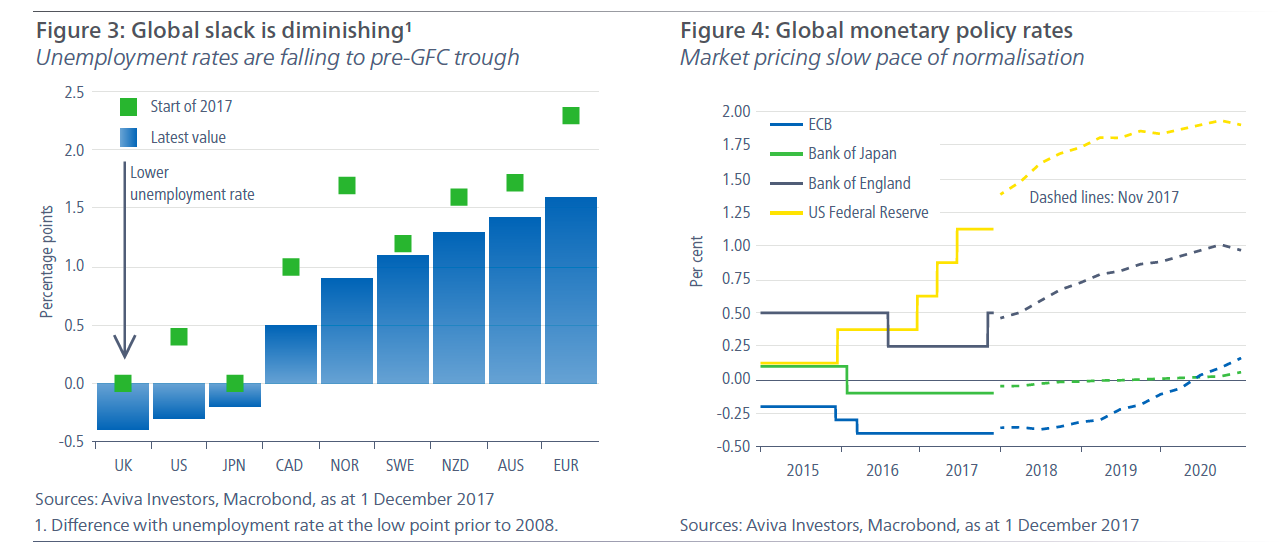

Over the course of 2017 above-trend growth across the major developed economies saw unemployment rates decline further. As a result, unemployment rates in some economies, such as the US, UK and Japan are now below the levels seen prior to the global financial crisis. Even allowing for the possibility that the equilibrium rate of unemployment may have fallen since 2007, these economies are likely to be very near to full employment (Figure 3). Other economies, such as the Eurozone, are further behind in their expansionary phase, and as such continue to have a reasonable degree of spare capacity. However, with a similar rate of above-trend growth expected next year, the Eurozone is likely to have relatively little spare capacity by the end of 2018. As the degree of spare capacity has been eroded, central banks have begun to embark on policy normalisation. The Federal Reserve is likely to have raised rates five times in this cycle by the end of 2017. Looking ahead, the market is currently pricing little more than one more hike in the US in 2019 and beyond, compared to another six increases currently expected by the Fed (Figure 4). We think the market is under-pricing the risk of further rate hikes over the coming year and beyond. Other markets look more fairly priced in terms of short-term rates, with little prospect of the European Central Bank (ECB) or the BoJ raising the short-term policy rate in 2018.

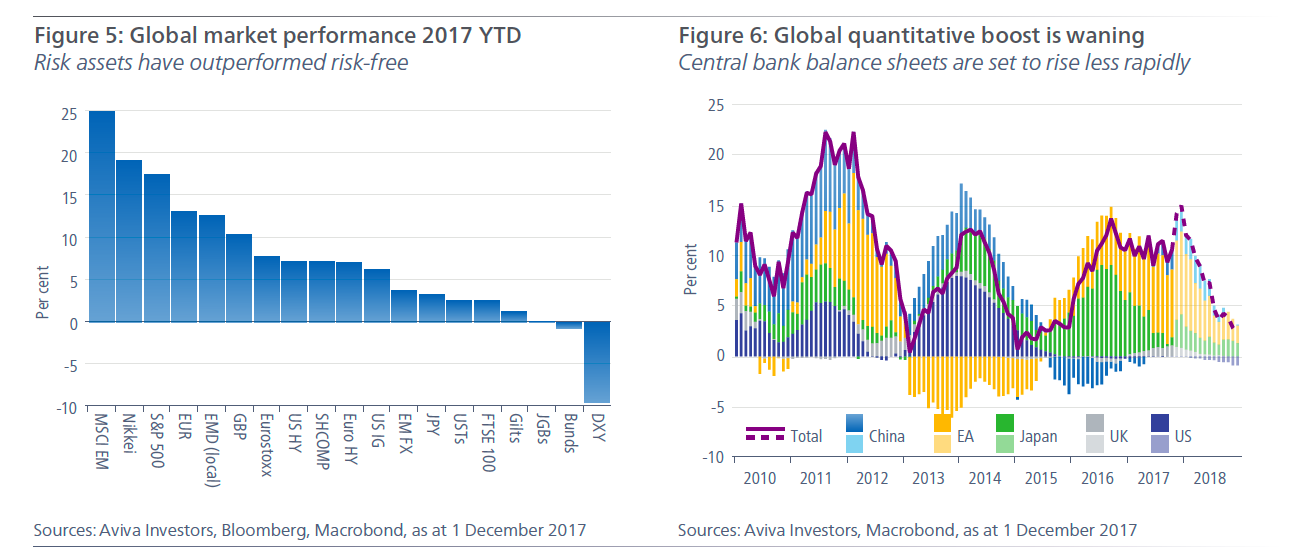

Expectations of stronger global growth and modestly higher inflation in 2018 provide the backdrop for a positive risk environment, just as they did in 2017 (Figure 5). Moreover, with the improvement in the global economy and the peak of monetary policy accommodation likely behind us, we would expect asset markets to be driven more by the underlying fundamentals than at any point in the past decade.

In terms of equity markets, that should mean a focus on the earnings outlook, valuations and sector allocations is likely to be increasingly important. The correlation between stocks within equity indices declined sharply in 2017, consistent with company fundamentals driving returns, rather than external risk factors. That increased dispersion of returns has also been a contributory factor to the decline in overall equity index volatility. Looking to 2018, we think that amongst the main regions, emerging market equities should benefit most from the improving global growth outlook, while also standing to gain from relatively lower valuations. Amongst developed markets, we expect Eurozone equities to be supported by continued above-trend growth and receding political concerns. We also think that Japanese equities present a good opportunity in 2018, with the potential for strong corporate profitability and a potential sea-change in corporate and household inflation expectations.

While we think that risk assets will be supported by economic growth, risk-free assets are more challenged. Arguably the most challenged is Eurozone government debt, where yields continue to be suppressed by ECB asset purchases. However, with a likely end to QE in September, we expect pressure on yields to start rising by the middle of 2018. Japanese government bonds are even more expensive, and could also be subject to a sell-off in 2018 if inflation rises above 1 per cent and the BoJ adjusts their target on YCC. If longer-term yields in these markets were to rise, then the pressure on global term premia would also increase, at a time when we expect the Federal Reserve to continue raising rates and reduce their balance sheet. Indeed, the liquidity and credit support globally from central bank balance sheets is likely to fall materially over the course of 2018 (Figure 6). That could be the catalyst for a normalisation in term premia and a more sustained rise in yields. However, there are likely to be some countervailing forces on yields, such as the demand for increased duration from Asia.

Investment grade corporate credit in both the US and Europe is also likely to be challenged in 2018 given the spread tightening seen over the past year and our views on the risk to duration. In Europe there is the added risk associated with the expected end of ECB purchases later in 2018. High yield credit is relatively more attractive given the potential for some further narrowing in spreads and the low probability of a material default cycle starting in 2018. Indeed default rates are expected to decline further over the next 12 months. The prospects for emerging market (EM) debt are also encouraging, with improved fundamentals and attractive valuations more than compensating for a rise in US rates. That said, recent months have seen heightened idiosyncratic risks, highlighting the potential for greater volatility across the EM debt spectrum, particularly with numerous elections taking place in 2018. A more cautious stance is warranted on EM hard currency (dollar-denominated) debt, where valuations look more stretched.

Finally, we think that global reflation will continue to favour currencies that are under-valued on a longer-term basis. That means the US dollar's peak is likely behind us, absent a more aggressive move by the Federal Reserve to tighten policy. The main beneficiary of the benign global environment ought to be emerging market currencies, although as with EM debt, idiosyncratic factors will dominate in some instances. We see the better performance as likely to be in India and Indonesia, with South Africa and Turkey more challenged. We expect the major G10 currencies to be relatively range-bound in 2018, with the euro likely to perform a little better on stronger domestic factors. Sterling remains vulnerable to Brexit negotiations, but could equally outperform if it looks likely there will be a long transition period agreed.