CITY AND EAST LONDON

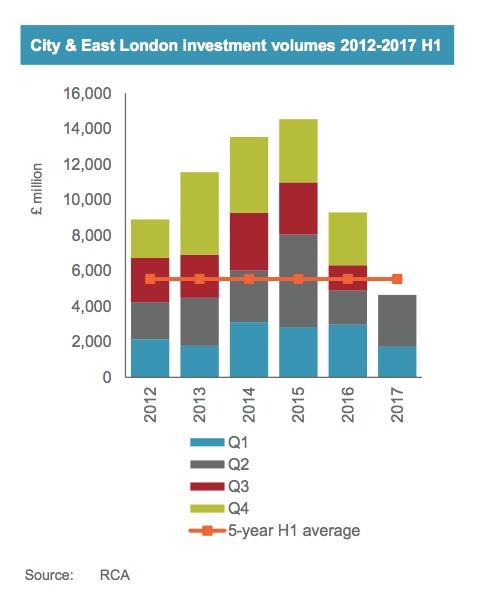

Investment activity in the City held up well during the first half of the year. An estimated £4.65 billion was transacted in H1 2017 compared to just over £4.0 billion in both H1 and H2 2016. East London in comparison has yet to see any transactions and as a result total volumes for the City and East London were below the same point last year.

The demand for large lot sizes continued apace during Q2, with a further six transactions in the £100 million plus lot sizes. This was on a par with the previous quarter. All bar one property of this size was purchased by overseas investors, the exception being Workspace’s acquisition of Salisbury House, 28-31 Finsbury Circus. The average lot size stands at just over £98 million for 2017, up from £50 million for the same period in 2016.

European investors returned to the City investment market in H1 2017, with both Q1 and Q2 recording in excess of £800 million of acquisitions. This was in part due to the purchase of Cannon Place by Deka (£485 million) and 2 & 3 Bankside to Deutsche AM (£310 million) in Q2 following closely on the back of Antirion’s purchase of Principal Place and HB Reavis’s acquisition of Elizabeth House in Q1.

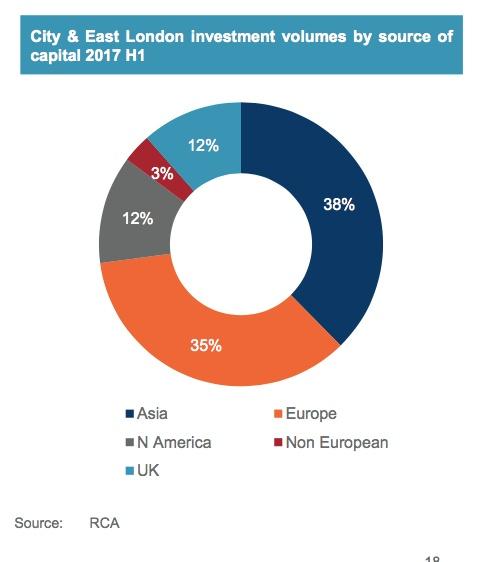

European investors accounted for 35% of investment volumes in H1, fractionally behind Asia who purchased 38% in the year to date. UK investors remain net sellers of c£2.0 billion, albeit influenced by the sale of The Leadenhall Building earlier in the year.

Funds and publically quoted companies were both the main purchasers and vendors in the year to date. Both institutions and private investors have been relatively quiet in comparison.

Prime office yields in the City and Midtown moved in by 25 bp to 4.00% as a result of the sheer weight of money targeting City properties. Looking forward prime yields are anticipated to hold at this level for the short to medium term.