EAST LONDON

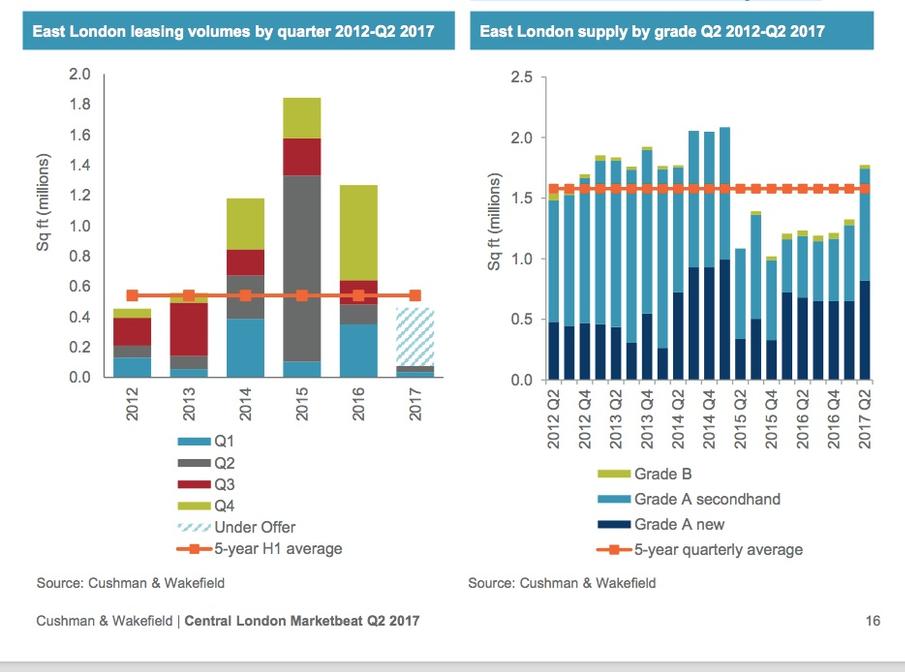

Following the substantial take-up levels in 2016, momentum slowed in 2017. Just 41,793 sq ft was let during Q2, which brought the H1 total for East London to 76,246 sq ft. This was 84% below the same point in 2016.

Nevertheless, the outlook is more positive with a further 383,000 sq ft of space under offer in East London at the end of June, a 61% increase on the volumes recorded in the previous quarter. This was bolstered by Cancer Research and the British Council under offer on 110,000 sq ft and 85,000 sq ft respectively at Building S9, The International Quarter, E20. As such leasing activity is anticipated to pick up into the latter part of 2017.

In addition, demand for space in East London remains strong with a number of large requirements currently circulating the market, such as further space for WeWork (70,000 sq ft), BGC (100,000 sq ft) and HMRC (300,000 sq ft).

Availability increased over the quarter to stand at 1.77 million sq ft, reflecting an availability ratio of 8.38%. Total available space exceeded the five-year average of 1.58 million sq ft for the first time since Q1 2015.

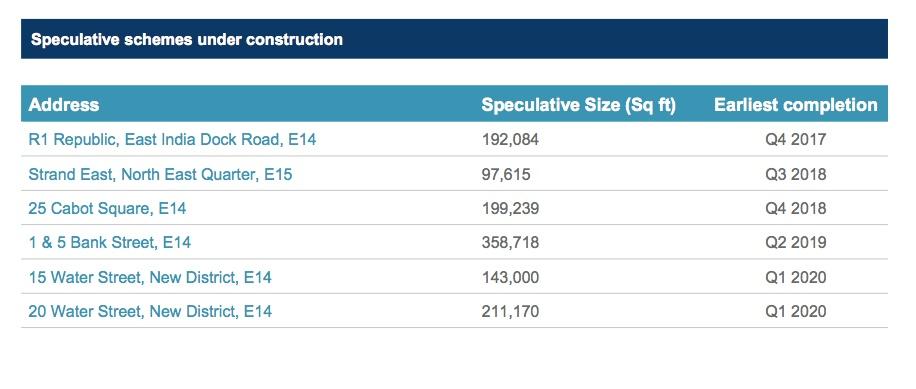

There was an increase of second hand space during the quarter, now standing at 952,000 sq ft, which accounts for over half of total space available. This trend was driven by tenant released space in buildings such as 15 Westferry Circus (170,000 sq ft) and 40 Bank Street (57,000 sq ft). There are currently seven buildings across East London which can accommodate a requirement in excess of 100,000 sq ft: the largest is R1 Republic, E14 which provides 192,000 sq ft and is due for completion in Q4 2017.

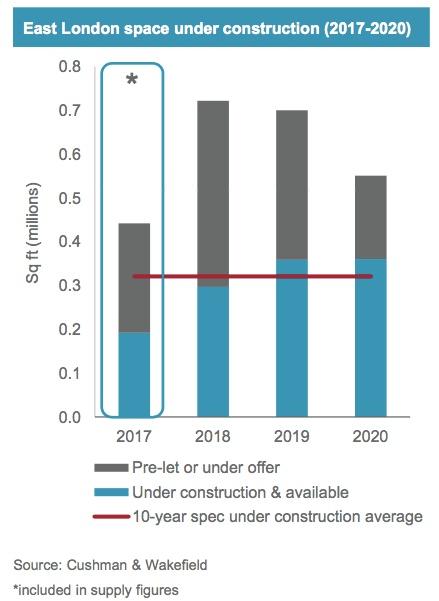

At the end of June, there was 1.0 million sq ft of speculative space under construction due to complete between 2018-2020, with a further 1.0 million sq ft of space which was either pre-let or under offer. The proportion of committed space under construction (50%) was higher than the Central London average of 45%. As such any significant uplift in future new supply is not anticipated to be as a result of the pipeline.

There were six schemes speculatively under construction across East London at the end of June: of which the largest is 1 & 5 Bank Street, E14 (359,000 sq ft remaining available) due to complete in 2019.

The New District phase of Canary Wharf is also underway, with two office buildings under construction – 15 Water Street (143,000 sq ft) and 20 Water Street (211,000 sq ft). As most of these new buildings will be added to the stock figures, the impact on vacancy rates will be moderated.

Speculative space under construction