Turnover increased by 17% to £4.3 billion (2015: £3.65 billion), with strong growth from new and used cars. The acquisitions of Knights and Drayton contributed £131 million of turnover following their acquisition in August and November. Gross profit of £504 million increased by £52 million compared to the previous year, with the growth coming from new and used cars as well as £14.5 million from acfquisitions. The gross margin of 11.8% was slightly lower compared to the prior year of 12.4%, due to a greater proportion of gross profit coming from the increased volume of car sales, which have a lower percentage margin than parts and aftersales.

The operating margin was slightly lower than last year at 2.2% (2015: 2.4%) and overheads increased by £37.1 million in the year, primarily due to the higher turnover and acquisitions in the period. *Adjusted operating profit from operations increased by 10% to £94.7 million (2015: £85.9 million).

Net interest costs increased by 27.5%, to £17.6 million (2015: £13.8 million) due to interest on pursuing our acquisitive strategy, including the acquisition cost of Ben eld last year and interest incurred in the Ben eld business. Higher levels of working capital, a large proportion of which were due to the acquisitions, were also a factor contributing to the higher interest charge.

Interest on group borrowings is based on floating interest rates together with interest rate hedges, where we have £30 million of hedges which were established in 2007 at an average rate of 5.1%, when interest rates were significantly higher than current levels. These increase the total interest charge so that we do not get the full benefit of the low UK base rate which has now been applicable for nine years.

Key financial highlights are summarised below:

• *Adjusted profit before tax for the year increased by 7% to £77.1 million, from £72.1 million last year, which is the highest trading result to date for the company;

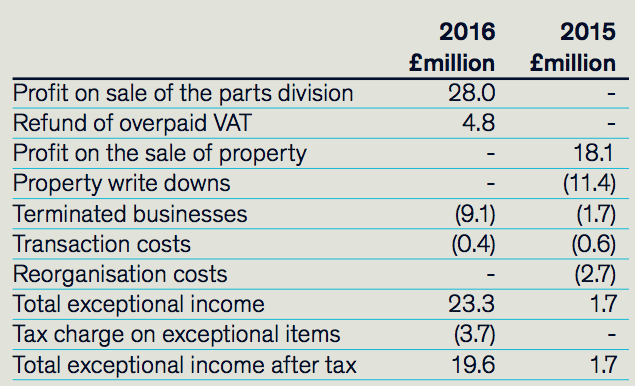

• Profit before tax was £91.8 million compared to a profit before tax in the previous year of £62.8 million, an increase of 46%. This includes net exceptional income of £23.3m which is explained in further detail below;

• Profit after tax was £81.3 million, an increase of 61% compared to £50.8 million in 2015; and

• Earnings per share increased by 59.2% to 20.51p compared to 12.88p in the prior year and *adjusted earnings per share of 15.87p compared to 15.24p in the prior year, an increase of 4.1%.

The tax charge for the year is £10.5 million (2015: £12 million) and reflects a charge of 11.4% of profit before tax. This is significantly lower than the standard rate of Corporation Tax for the year of 20%. This is due to two factors: the first is the reduction in the deferred tax liability due to a future reduction in the rate of Corporation Tax to 17%. This creates a one off benefit of approximately £4 million which is reflected in the current year tax charge.

The second relates to the taxation of the sale of the Battersea property in last year’s accounts where Corporation Tax of £3.4m was provided. This is subsequently not required as the gain on the sale of the property is covered by roll over relief and the tax provision reversed this year, which reduced this year’s tax charge by £3.4m.

Exceptional items in the year consist of the following and there has been a significant level of exceptional profit included in profit before tax which predominantly relates to the sale of the parts division in the year.

Cash generated from operations for the year was a large increase compared to the prior year at £140.9 million (2015: £67.9 million). Net working capital reduced by £33.3 million (2015: increase of £32.7 million). Stock increased by £23.4 million but this was more than offset by positive movements in debtors which reduced by £27.6m and creditors which increased by £93.2 million.

Capital expenditure was £36.3 million (2015: £35.2 million) and proceeds from the sale of properties and dealership businesses was £28.9 million (2015: £9.8 million), so net capital expenditure was £7.4 million (2015: £25.4 million). The majority of capital expenditure was on new or improved premises for dealerships and the increase compared to the previous year reflects our ongoing commitment to improve our retail premises so they reflect modern and state of the art facilities, as we signalled in our annual report last year.

As referred to in the Strategic and Operational Review, expenditure on acquisitions during the year relates to the acquisitions of Knights on 22 August 2016 for a cash consideration of £26.6 million and Drayton on 4 November 2016 for a cash consideration of £56.3 million. The sale of the parts division on 4 November 2016 resulted in gross sale proceeds of £126 million, including £9.1 million for the freehold properties used in the business.

The strong operational cash ow allowed us to make further reductions in bank loans where loan repayments of £10.2 million were made during the year compared to £11.8 million last year. New loans of £14.0 million relate to the loans acquired with the Knights business which were funding the freehold properties. We had intended to lease these properties as the interest rate on the loans was significantly above the market rate. However, we negotiated a reduction in the interest rate and it was therefore sensible to retain these loans at the reduced rate of interest.

Net debt reduced by £87.6 million due to the strong operational cash ow but also as a result of the proceeds from the sale of the parts division exceeding the amount spent on the acquisitions of Knights and Drayton. This reduction in net debt resulted in net borrowings of £74.1 million at 31 December 2016 compared to £161.7 million at the start of the year, net debt being calculated as gross bank borrowings less cash balances.

Our bank facilities were renewed and increased on 2 September 2015, at the time of and to fund the acquisition of Ben eld. The facilities were also extended for two years to March 2020 and were agreed with a group of six banks: Bank of Ireland, Barclays, HSBC, Lloyds, RBS and Yorkshire Bank. The facilities consisted initially of a term loan of £100 million, which has since reduced to £85.0 million and a revolving credit facility of £150 million.

There is also the potential to increase the term loan by up to an additional £30 million to fund future acquisitions. Interest is charged on both loans at a margin of between 1.2% and 2.15% above LIBOR, depending on the ratio of net bank debt to EBITDA. These facilities are subject to half yearly covenant tests on interest cover and net bank debt to EBITDA. The covenant tests are set at levels that provide sufficient headroom and flexibility for the group until maturity of the facilities in March 2020.

At 31 December 2016, total facilities were £235.0 million (2015: £245.0 million) of which £74.1 million, net of cash balances, was being utilised, leaving unutilised facilities of £160.9 million. These bank facilities, together with the group’s strong operational cash ow, indicate that the group has sufficient facilities available to fund its operations and allow for future expansion.

At 31 December 2016, gearing was 22% compared to 54% at 31 December 2015 and net debt to EBITDA was 0.66 compared to 1.61 last year. The group’s underlying profitability and strong cash ow should result in further reductions in borrowing in the future and help ensure that the level of borrowing remains under control and is at a reasonable level in relation to net assets.

The group has a policy of investing in freehold and long leasehold property as the preferred means of providing premises for our car dealerships, where possible. As a result, we have a significant and valuable portfolio of freehold and long leasehold properties, where the net book value at 31 December 2016 was £287.7 million compared to £252.4 million last year. Short leasehold properties had a value of £4.6 million (2015: £5.9 million).

In our interim report, we indicated that due to the encouraging results and strong financial position of the group, the interim dividend would be increased by 20% to 1.28p per ordinary share and this was paid on 25 November 2016. We are now proposing a 15% increase in the final dividend to 2.36p per share (2015: 2.05p), giving a total dividend for the year ended 31 December 2016 of 3.64p per share (2015: 3.12p), representing an annual increase of 17%.

The dividend has now increased by over 100% compared to the dividend payable for the year ended 31 December 2010 and continues our policy of increasing the dividend provided there is satisfactory growth in profitability.

The increase in the total dividend this year recognises that the dividend cover has risen significantly due to the continued increase in profits of recent years. The Board has taken the decision that the level of cover should reduce over the medium-term to a level of between 3.5 and 4.0 times. However, the board will continue to review the dividend policy in the light of the company’s trading performance whist retaining sufficient cash ow to fund future expansion in terms of both organic growth and acquisitions.

The final dividend of 2.36p per share is subject to shareholder approval at the Annual General Meeting and will be payable on 31 May 2017. The ex-dividend date will be 4 May 2017 and the record date will be 5 May 2017. This will represent a cash out ow of £9.3 million, which gives a total dividend for the year of £14.4 million (2015: £12.3 million). Dividends paid in cash during the year were £13.2 million, an increase of 13.8% compared to the previous year.

The group has operated two de ned benefit pension schemes for a number of years, The Lookers Pension Plan and The Dutton Forshaw Pension Plan. We also acquired another de ned bene t pension scheme with the acquisition of Ben eld. However, the Ben eld scheme is reasonably well funded and there is a modest surplus in the 2016 accounts in relation to the Ben eld pension scheme. All three schemes are closed to entry for new members and also closed to future accrual. Whilst the asset values of the Lookers and Dutton Forshaw schemes have increased by £26.6 million during the year, the valuation of the liabilities has increased by £49.7 million due to the significant reduction in the yield of UK Government bonds, following the EU referendum.

As a result, the net de cit included in the balance sheet increased by £23.1 million, although there is a deferred tax asset which reduces this by £3.9 million. However it is important to appreciate that the assessment of valuation of

the pension schemes is based on several key assumptions prescribed by accounting standards and over which the directors have no control. As a result, the calculation which estimates the potential liabilities of the schemes can increase or decrease the liabilities due to factors that have no relation or relevance to the trading results of the group.

The impact of these factors is that the combined value of the deficits of both schemes increased in the year and the total de cit after deferred tax is now £65.1 million (2015: £44.2 million). Relatively small changes in the bases of valuation can have a significant effect on the calculated de cit hence the movement in the calculated de cit can be subject to high levels of volatility. The board continues to look at its options to reduce both the annual cost of operating both schemes and what actions can be taken to reduce the de cit on the schemes, thereby reducing exposure to movements in these liabilities and reducing the de cit over the medium and longer term.